Portfolio

Multi-Factor ML/RL Strategy, Agentic Research & Orchestration Pipeline

Core Components

Multi-Factor, ML & RL Strategy Research

LightGBM-based signal fusion over a multi-factor alpha library (value, momentum, quality, low-vol, cross-sectional microstructure), with RL policies for allocation and execution. Factors are scored by IC, decile spreads, and turnover-adjusted Sharpe. Every strategy is cross-validated on both vectorbt and QuantConnect Lean to eliminate framework-specific artifacts.

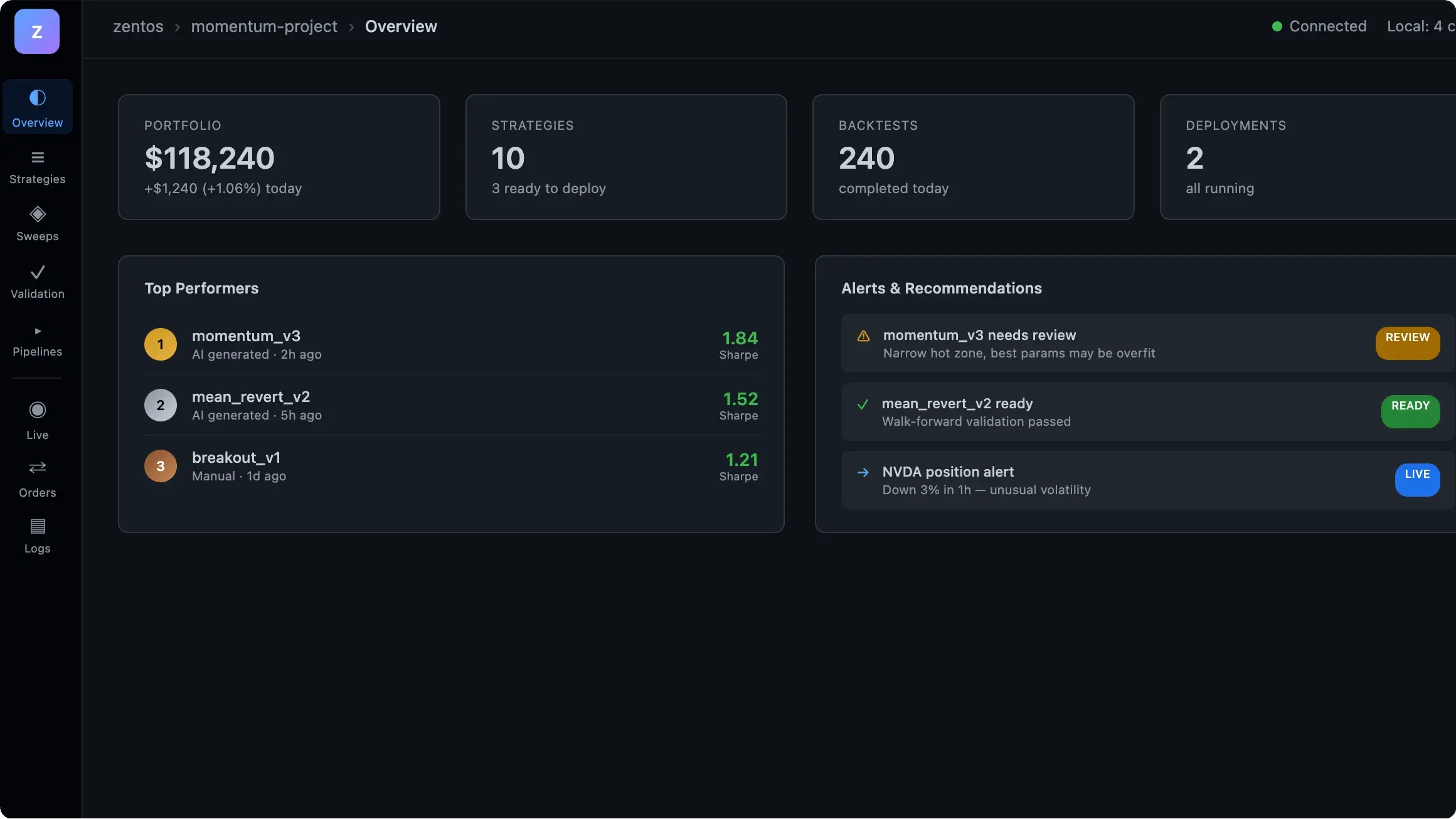

Zentos CLI — End-to-End Agentic Pipeline

Shipped Zentos CLI, an end-to-end agentic pipeline that lets external quantitative researchers and developers submit strategies to the platform without touching infrastructure. Natural-language research intent is compiled into declarative StrategySpec objects; the CLI orchestrates data staging, sandboxed Python execution (Docker, no network, read-only fact copy), the full validation gate, and deployment to live brokers. The goal is to compress the research-to-production loop from weeks to hours while preserving point-in-time safety, reproducibility, and auditability at every step.

LLM Agents in the ML/DL Strategy Stack

Integrated LLM agents as a productivity layer on top of an otherwise deterministic ML/DL strategy platform, scoped to three production use cases: (1) model routing — selecting between LightGBM, deep-learning, and RL policies based on regime classifiers and factor exposures; (2) factor mining — proposing, implementing, and backtesting candidate alpha formulas under human-in-the-loop review; (3) research assistance — summarizing 10-K and earnings transcripts, surfacing related literature, and drafting strategy post-mortems. Agents orchestrate and propose — all signals, weights, and orders remain under deterministic control.

Previous Experience

MLOps Platform & Federated Learning SDK

- Collaborated with ML researchers and engineers to productionize FedML Federate—a zero-code, cross-platform federated learning SDK deployable on edge GPUs, smartphones, and IoT devices.

- Drove product roadmap for TensorOpera Deploy (model serving), GPU cloud pricing, and monitoring infrastructure from 0-1.

- Translated cutting-edge research into user-facing MLOps tools, bridging the gap between research prototypes and production-grade deployments.

ML Platform & Privacy Computing

- Designed EAS (Elastic Algorithm Service) deployment module with blue-green release and pricing features, enabling ML model deployment as inference services with auto-scaling, canary releases, and real-time monitoring.

- Led federated learning privacy computing module design and national security compliance assessment.

CV Defect Detection Engineering

- Collaborated with CV researchers to productionize defect detection models for ultra-small precision instrument quality inspection.

- Built data pipelines for batch processing and edge annotation of thousands of multi-angle instrument images.

- Tranformed research prototypes & models into production-grade deployments and benchmarked detection accuracy.

Research Interests

Focus: Making agentic systems a rigor-preserving layer in quantamental research — not a shortcut around it. Concretely, how declarative strategy specs, sandboxed execution, and LLM agents as orchestrators (not oracles) can let external contributors ship validated alpha without compromising point-in-time safety, reproducibility, or the deterministic ML/RL decisions behind every trade.